When it comes to plumbing in Colorado, homeowners often wonder what their insurance will cover. Colorado’s cold winters and fluctuating weather can cause all kinds of plumbing issues. Burst pipes, leaking water heaters, and backed-up sump pumps are common problems around here, but navigating what’s covered by insurance can be tricky. In this guide, we’ll walk you through the basics of what homeowners insurance typically covers when it comes to plumbing, with a focus on the unique conditions we face here in Colorado.

The Short Answer: Will Homeowners Insurance Cover Plumbing in Colorado?

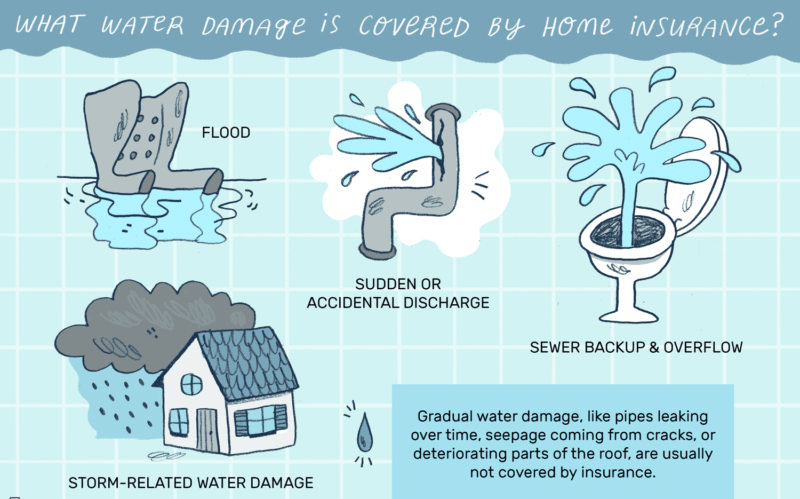

In most cases, yes, homeowners insurance will cover sudden and accidental plumbing damage, such as burst pipes or appliance leaks. However, it won’t cover gradual wear and tear, negligence, or flooding. If you live in Colorado, where freezing pipes are a risk, additional coverage options might be worth considering.

Understanding What’s Covered by Homeowners Insurance in Colorado

Let’s break down what’s typically covered by homeowners insurance when it comes to plumbing. First off, the key thing to remember is that insurance generally covers sudden and accidental damage. For example, if you’ve got a pipe that freezes and bursts in the middle of a Greeley winter, most policies will cover the damage that pipe causes. They’ll help you pay to repair the walls, floors, and any other damage caused by the water. Just don’t expect them to replace the pipe itself—that’s usually on you.

Same goes for appliance leaks. If your water heater or dishwasher decides to dump water all over the place unexpectedly, insurance will likely cover the clean-up and repairs, as long as you’ve been maintaining things properly. The key word here is “sudden”—if it’s a slow leak that you’ve ignored, or a problem that’s been creeping up for a while, don’t count on your insurance to help.

Finally, there’s the issue of overflowing sinks and toilets. If your kid leaves the faucet running and floods the bathroom, you’re usually covered. However, if the overflow is caused by a long-term blockage, it gets trickier. Always check your policy for those fine details.

What’s Not Covered by Standard Policies

Now, let’s talk about what isn’t covered by your average homeowners insurance policy, and this is where we see a lot of confusion. If damage happens because of neglect—like you didn’t insulate your pipes during the winter, and they freeze—that’s on you. Insurance companies will often deny claims if they think you could’ve prevented the damage by being proactive.

Gradual damage is another area where people get tripped up. If you’ve got a pipe that’s been slowly leaking for months, causing mold or rot, that won’t be covered. The insurance company expects homeowners to stay on top of maintenance, and if they think you’ve ignored a problem for too long, they won’t pay out.

Another big exclusion is flooding. Now, we know Colorado isn’t the first place people think of when it comes to floods, but between spring snowmelt and occasional heavy rains, it happens. Standard policies don’t cover flood damage—you’ll need a separate flood insurance policy for that.

Finally, sump pump failures and water backups aren’t usually covered unless you’ve added that specific coverage to your policy. This is something we always recommend to our customers because it’s a relatively small cost to protect against a potentially huge mess.

Special Considerations for Colorado Homeowners

Colorado’s climate presents some unique plumbing challenges, and that’s something you really need to keep in mind when looking at insurance coverage. The big one? Winter weather. When temperatures drop, pipes freeze, and if you’re not careful, they’ll burst. A common mistake we see is people leaving for a weekend trip and setting their thermostat too low to save energy. If your pipes freeze because of that, good luck with the insurance claim—most policies will deny it because they consider it negligence.

Older homes in places like Greeley or Fort Collins are also more prone to plumbing issues. Homes built before the 1980s often have outdated systems that can spring leaks or clog easily, and insurance won’t cover damage if they decide your pipes were due for replacement.

Finally, consider adding water backup coverage. Colorado homes with basements are at risk for water backups from sump pump failures during snowmelt or heavy rains. This extra coverage can save you from footing a massive bill if the worst happens.

How to File a Plumbing Insurance Claim in Colorado

Filing a plumbing insurance claim in Colorado can be straightforward if you follow the right steps. First, document the damage immediately—take photos or videos of everything, even if it’s messy. This will help when you’re dealing with the adjuster later. Next, stop further damage—if water is still flowing, shut off the main valve. Insurance companies expect you to take reasonable steps to prevent more damage after the initial incident.

Call a licensed plumber right away to assess the damage and provide a report. A local plumber familiar with Colorado conditions (like those at Origin) will know what insurance companies need in terms of documentation. Then, contact your insurance company as soon as possible to file the claim. The faster you report it, the smoother the process will go. When the adjuster comes, be ready to explain what happened and show your documentation. Following these steps can make a stressful situation a bit more manageable.

FAQs

Here are a few of the most common questions we get from homeowners about plumbing and insurance:

Does homeowners insurance cover pipe replacement?

Generally, no. Most policies will cover the damage caused by a burst pipe—like wet drywall or ruined floors—but they won’t pay for the pipe itself. For that, you’d need equipment breakdown insurance, which is an add-on.

What if my basement floods from a burst pipe?

If a burst pipe floods your basement, your homeowners insurance should cover the damage as long as the pipe broke suddenly. But, and this is important, if your sump pump fails, that’s not covered unless you’ve added water backup coverage. We always recommend this add-on if you’ve got a basement, especially in places like Greeley where we get heavy snowmelt and rains.

Will insurance cover mold from a leaky pipe?

Only if the leak was sudden and unexpected. If the mold is from a slow, long-term leak, your claim will likely be denied.

A Few Extra Tips on Colorado Homeowners Insurance and Plumbing

At the end of the day, understanding your homeowners insurance policy is key to making sure you’re covered when plumbing problems strike. Here in Colorado, especially with our unpredictable weather and older homes, it’s important to know what’s in your policy and what add-ons might make sense, like water backup or equipment breakdown coverage. Take preventative steps—insulate your pipes, keep your home heated, and stay on top of maintenance. And most importantly, talk to your insurance provider to make sure you’re protected before anything happens. Trust us, it’s better to know now than when you’re ankle-deep in water!